Labuan Malaysia Country-by-Country Reporting Guidelines

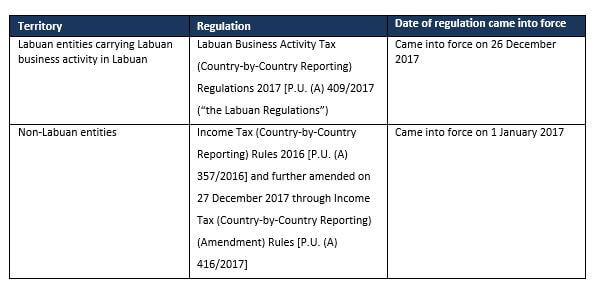

On 26 December 2017, Malaysia Inland Revenue Board (“IRB”) gazetted the Country-by-Country reporting (“CbCR”) regulations for Labuan

entities. The implementation of CbCR will take effect for the financial year starting on and after 1 January 2017. On 1 January 2019, IRB

published CbCR Guidelines for Labuan entities.

In Malaysia, CbCR is governed by two separate regulations as follows:

Labuan is a Federal Territory of Malaysia that maintains its own independent corporate laws and taxation regime from the rest of Malaysia.

How can we help?

Labuan Malaysia Country-by-Country Reporting Guidelines 2019 require careful attention and compliance from multinational enterprises (MNEs)

operating in Labuan. We offer comprehensive services to ensure that your CbCR obligations are met efficiently and accurately. With our

support, you can navigate the complexities of CbCR in Labuan confidently, ensuring compliance and minimising risks associated with

non-compliance.

Our services include:

CbCR in Labuan

With our support, you can navigate the complexities of CbCR in Labuan confidently, ensuring compliance and minimizing risks associated with

non-compliance.

Malaysia’s transfer pricing framework continues to evolve, with the Inland Revenue Board of Malaysia applying increasing scrutiny to how

multinational groups price, document and defend related‑party transactions. For businesses operating in Malaysia, transfer pricing has

become a core tax risk area rather than a routine compliance exercise.

The Global Minimum Tax in 2026: Why Pillar Two Matters More Than Ever in a Fractured World

As tariff wars intensify, government deficits balloon, and supply chains fragment, the OECD’s 15% global minimum tax has shifted from a

technical compliance issue to a strategic imperative reshaping how and where multinational enterprises compete.

TPS Asia and Malaysia Recognised in 2026 ITR World Tax Rankings

We’re thrilled to announce that Transfer Pricing Solutions Asia (Singapore) and Transfer Pricing Solutions

Malaysia

have both been ranked as recommended Transfer Pricing firms in the 2026 ITR World Tax rankings.